Life insurance is a crucial component of financial planning, offering not only protection for loved ones in the event of one's passing but also, in some cases, a savings component known as cash value. Understanding cash value in life insurance policies is essential for policyholders who want to maximize their financial strategy. This article demystifies the concept of cash value, examining its accumulation, benefits, risks, and the various ways it can be accessed and utilized within permanent life insurance policies.

Key Takeaways

Cash value is a unique feature of permanent life insurance policies, serving as a savings component that grows tax-deferred over time.

Premium payments in cash value policies are allocated to both the insurance cost and the savings component, enabling the cash value to accumulate.

Policyholders can access their cash value through withdrawals, loans, or policy surrender, each with distinct tax implications and financial consequences.

While cash value can offer financial flexibility and growth, it also comes with potential risks and costs that must be carefully evaluated.

Consulting with financial experts and comparing different cash value life insurance products can help individuals make informed decisions that align with their financial goals.

The Basics of Cash Value in Life Insurance

Defining Cash Value and Its Role in Permanent Policies

Cash value is a distinctive feature of permanent life insurance policies, serving as a financial reservoir that policyholders can tap into under certain conditions. It represents the savings component of a policy that accumulates value over time. This cash value grows tax-deferred, meaning taxes on the interest or investment gains are not paid until the money is withdrawn.

The role of cash value in permanent policies is multifaceted:

It can be used to pay premiums, effectively lowering the out-of-pocket cost for the insurance.

Policyholders may borrow against the cash value for loans, which can be used for various personal expenses.

In some cases, it can serve as an additional source of retirement income or fund long-term care needs.

While cash value adds a layer of financial utility to life insurance, it's important to weigh the benefits against the costs and potential impact on the death benefit.

Understanding the implications of cash value is crucial for policyholders, as it affects both the present financial flexibility and future benefits of the life insurance policy.

Types of Life Insurance Policies with Cash Value Features

Life insurance policies with cash value features are distinct from term life insurance, which lacks this component. Whole life, universal life, and variable life insurance are the primary types of permanent policies that include a cash value feature. Each type offers unique approaches to premium payments and cash value growth.

Whole life insurance guarantees a fixed premium and a cash value that grows at a predetermined rate.

Universal life insurance provides more flexibility with premium payments and cash value growth based on market interest rates.

Variable life insurance allows policyholders to invest the cash value in various investment options, which can lead to higher growth potential but also comes with increased risk.

Cash value is a crucial aspect of permanent life insurance, enabling policyholders to accumulate a tax-deferred balance that can be accessed during their lifetime. It's important to understand that in the early years, cash value growth is typically slow, but it accelerates over time, potentially offering a higher return.

Comparing Cash Value to the Death Benefit

Understanding the distinction between cash value and the death benefit is crucial in evaluating life insurance policies. The death benefit is the amount paid to beneficiaries upon the policyholder's death, while the cash value serves as a savings component that can be accessed during the policyholder's lifetime.

The cash value is not intended for beneficiaries and typically reverts back to the insurance company upon the policyholder's death. However, certain policies may offer both the death benefit and cash value, but at a higher cost.

Cash value can be utilized in various ways, such as reducing premium payments, supplementing retirement income, or covering unexpected expenses. It's important to note that the method of cash value payout can differ based on the type of policy. For instance, universal life policies may allow the cash value to be paid out as part of, or in addition to, the death benefit.

Mechanics of Cash Value Accumulation

How Premium Payments Contribute to Cash Value

When you purchase a cash value life insurance policy, your premium payments are allocated in several ways. A portion of each premium contributes directly to the cash value, which grows over time. This growth is tax-deferred, meaning you won't pay taxes on the gains as they accrue.

The allocation of premium payments can be broken down as follows:

Policy fees and charges

The cost of the insurance coverage

The cash value account

Depending on the type of policy, the cash value may earn a fixed interest rate or vary with market performance. It's essential to recognize that not all of your premium goes into the cash value; a significant part covers the insurance and associated fees.

Accessing the cash value can be done through withdrawals or loans, but these actions may affect the policy's benefits and the death benefit amount. It's crucial to understand the terms and potential consequences before utilizing the cash value.

The Impact of Interest and Investment on Cash Value Growth

The growth of cash value in a life insurance policy is significantly influenced by the interest rate or investment performance. Policies with a fixed interest rate provide a steady, predictable increase in cash value over time. In contrast, policies tied to investment performance can see more variable growth, often reflecting market conditions.

Your policy's interest rate or investment choices determine the rate of cash value accumulation.

Market-linked policies may have a minimum guaranteed return (floor) and a maximum growth cap (ceiling).

Comparatively, direct investments in stocks or mutual funds may offer higher returns but come with increased risk.

The balance between stability and potential for growth is a key consideration when evaluating the suitability of cash value life insurance as an investment.

It's important to understand that while some policies guarantee a minimum rate of return, others allow for participation in potentially higher gains from market performance, albeit with a ceiling to limit maximum growth. This structure aims to provide a level of protection against market volatility while offering the opportunity for cash value appreciation.

Understanding Policy Loans and Withdrawals

Policyholders have the flexibility to access their policy's cash value through loans and withdrawals, each with its own set of implications. Withdrawals reduce the death benefit by the amount taken out, as they are a direct removal of funds from the policy's cash value. This can be advantageous for immediate financial needs or significant life events, like purchasing a home.

Loans, on the other hand, allow policyholders to borrow against their cash value. These loans typically do not require a credit check and may offer lower interest rates compared to traditional loans. While not mandatory, repaying the loan is beneficial to maintain the policy's full death benefit. Failure to repay can result in a reduced death benefit, as the outstanding loan amount plus interest will be deducted.

The strategic use of policy loans and withdrawals can enhance the utility of a life insurance policy, making it a dynamic financial instrument.

It's crucial to understand the tax implications of these actions. Withdrawals are generally tax-free up to the amount of premiums paid, but loans are not considered taxable income. However, if the policy lapses with an outstanding loan, the amount exceeding the premiums paid may be taxed as income.

Advantages and Drawbacks of Cash Value Policies

The Financial Benefits of Building Cash Value

Building cash value within a life insurance policy offers a unique blend of financial security and wealth accumulation. The cash value acts as a savings component, growing over time and providing a range of benefits that extend beyond the traditional death benefit. Here are some of the key financial advantages:

Tax-deferred growth: The cash value in your policy grows without immediate tax implications, allowing your investment to compound more efficiently over time.

Loan collateral: You can borrow against the cash value of your policy, often at favorable interest rates, without disrupting the policy's death benefit.

Flexible use of funds: Access to cash value can provide financial support for various needs, such as supplementing retirement income or covering unexpected expenses.

The strategic use of cash value can significantly enhance your financial planning, offering a versatile tool for managing both present and future financial challenges.

It's important to note that while the benefits are substantial, they must be balanced against the costs and risks associated with cash value policies. Careful consideration and planning are essential to ensure that a cash value life insurance policy aligns with your long-term financial objectives.

Potential Risks and Costs Associated with Cash Value

While cash value life insurance offers a savings component and the potential for growth, it's important to be aware of the risks and costs involved. Policies with cash value are generally more expensive than term life insurance, as a portion of your premium goes towards building the cash value.

More expensive premiums: The cost of premiums is higher compared to term life insurance.

Interest and tax complications: Loans against the cash value may incur interest and create potential tax liabilities.

Reduced death benefit: Taking out loans against the policy can reduce the death benefit available to beneficiaries.

Growth takes time: Building a significant cash value can take many years, and early withdrawals may have financial penalties.

It's crucial to consider these factors in the context of your overall financial plan and to consult with a financial advisor to determine if a cash value policy aligns with your goals.

Evaluating the Suitability of Cash Value Life Insurance for Your Financial Goals

When considering cash value life insurance, it's essential to assess how well it aligns with your financial objectives. This type of policy combines a death benefit with a savings component, allowing the cash value to grow over time. Here are some factors to consider:

Long-term financial goals: Is building a tax-deferred savings account for retirement or future expenses important to you?

Financial flexibility: Do you value the option to borrow against the policy or make withdrawals during your lifetime?

Costs versus benefits: Are the potential growth and the financial benefits worth the typically higher premiums compared to term life insurance?

It's crucial to understand that cash value life insurance is not merely an expense but an investment in your future financial security. However, it's not suitable for everyone, and the decision should be based on a thorough analysis of your individual circumstances.

Before making a decision, consider speaking with a financial advisor to determine if a cash value policy makes sense for you. They can help you weigh the pros and cons, taking into account your unique financial situation and goals.

Accessing Your Policy's Cash Value

Options for Withdrawing Cash Value

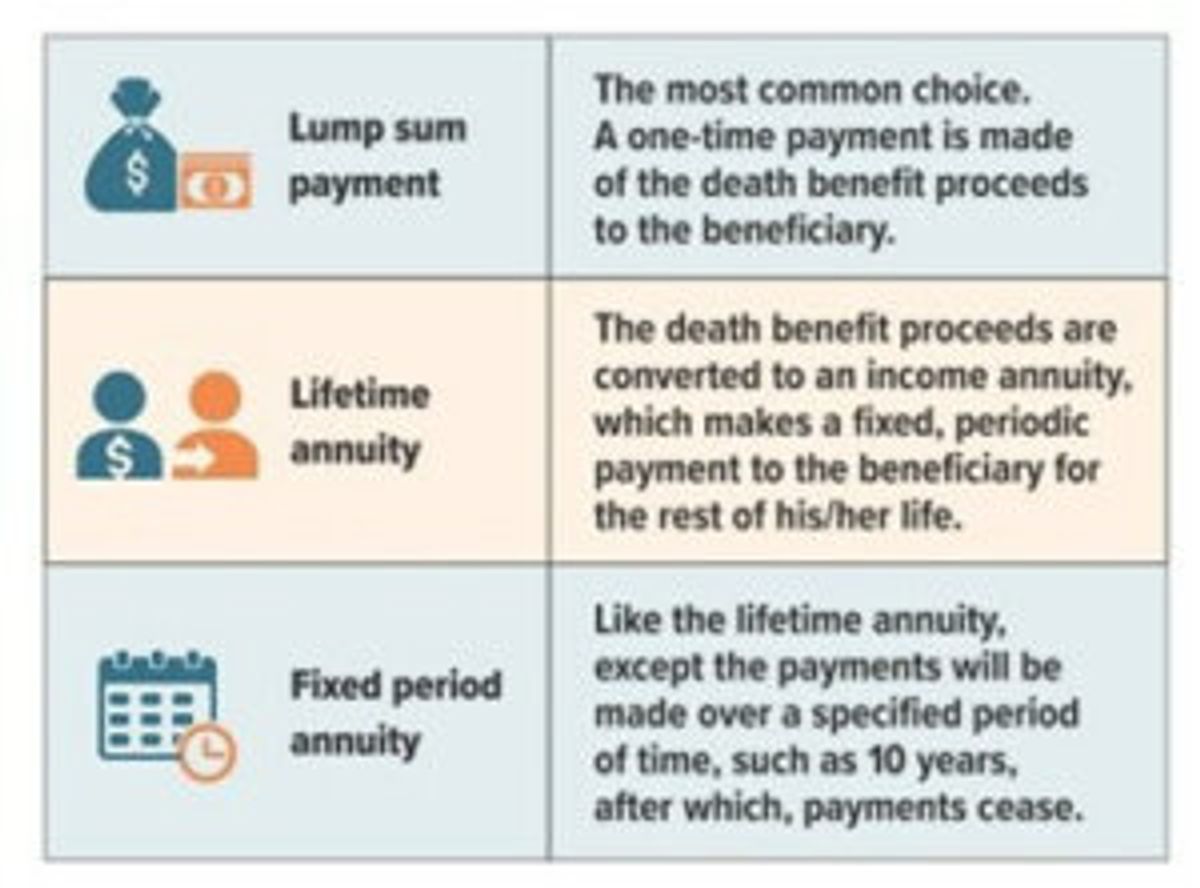

Policyholders have several avenues to access the cash value of their life insurance policies. Withdrawing funds directly is a straightforward method, allowing you to use the cash for any purpose, from emergency expenses to planned investments like a home down payment. However, it's crucial to remember that such withdrawals can reduce the remaining death benefit.

Another common option is to take out a loan against the cash value. This approach provides liquidity without an immediate reduction in the death benefit, but it does come with the obligation to repay the loan with interest. Failure to repay can lead to a decrease in the death benefit or policy lapse.

Policyholders may also use their accumulated cash value to cover premium payments, which can help maintain the policy without out-of-pocket expenses.

Lastly, full or partial surrender of the policy is possible, though this often comes with tax implications, especially if the withdrawal amount exceeds the premiums paid.

The Tax Implications of Accessing Cash Value

When you access the cash value of your life insurance policy, the tax implications can vary based on the method and amount you withdraw. Withdrawals up to the amount of premiums paid are generally not taxable. However, amounts exceeding the premiums paid are subject to income tax.

Scenario 3: Withdrawing partially or fully may result in taxes on the excess over premiums paid.

Scenario 4: Using cash value to pay premiums is typically not taxable.

The cash value in a life insurance policy grows tax-deferred, meaning you won't owe taxes on the growth until you withdraw the funds. It's crucial to understand that policy loans and withdrawals reduce the death benefit and may take a considerable time to build up, potentially affecting the long-term value of your policy.

Strategies for Maximizing Your Policy's Cash Value Potential

To enhance the growth of your policy's cash value, consider these strategies:

Regularly review your policy's performance to ensure it aligns with your financial goals. Adjust your investment choices in variable policies to respond to market conditions and optimize returns.

Reinvest dividends back into your policy to increase the cash value.

Use the cash value to pay premiums, which can help sustain the policy and continue its growth without out-of-pocket expenses.

By strategically managing your policy, you can leverage the cash value as a tool for wealth building and financial planning.

Remember, the cash value of your policy can serve multiple purposes. It can be used to supplement retirement income, cover long-term care costs, or even reduce your premium payments. The key is to balance the use of cash value with the preservation of the death benefit for your beneficiaries.

Making an Informed Decision on Cash Value Life Insurance

How to Assess Different Cash Value Life Insurance Products

When evaluating cash value life insurance products, it's crucial to understand the nuances that differentiate one policy from another. Consider the policy's flexibility, such as the ability to adjust premium payments and the ease of accessing cash value. Assess the investment component, which can significantly influence the growth of the cash value over time.

Review the types of policies available: whole life, universal life, and variable life insurance.

Compare the interest rates or investment returns each policy offers.

Examine the fee structure, including premiums, administrative fees, and potential penalties for early withdrawal.

It's essential to align the policy's features with your long-term financial objectives, ensuring it complements your overall financial plan.

Finally, scrutinize the insurer's financial strength and reputation, as this will impact the security of your investment. Policies should be compared not just on their projected cash value growth, but also on the company's track record of reliability and customer service.

Consulting with Financial Experts on Cash Value Benefits

When considering cash value life insurance, consulting with financial experts can provide clarity and confidence in your decision. Experts can tailor advice to your unique financial situation, ensuring that the policy aligns with your long-term goals and investment strategy. They can help you understand complex policy details, such as fees, surrender charges, and the implications of loans and withdrawals on your policy's value.

Evaluate your financial goals and needs

Analyze the long-term performance of different cash value policies

Consider tax implications and potential risks

Develop a strategy for integrating the policy with your overall financial plan

Financial experts can offer insights into how cash value life insurance fits into a diversified portfolio and its role in estate planning. Their guidance is invaluable in navigating the nuances of these policies and in making an informed decision that benefits your financial future.

Real-life Examples and Case Studies of Cash Value Utilization

Understanding how cash value in life insurance works in real-life scenarios can provide valuable insights into its practical benefits and applications. Case studies often reveal the versatility of cash value, demonstrating how individuals can use it to address various financial needs throughout their lifetimes.

John Doe, at age 45, borrowed against his policy's cash value to fund his child's college education, avoiding the need for student loans.

Jane Smith, a retiree, supplemented her income by making systematic withdrawals from her policy's cash value, thus maintaining her lifestyle without depleting other retirement savings.

The Johnson Family Trust utilized the cash value of their policy to settle estate taxes, ensuring a smooth transfer of assets to beneficiaries.

The strategic use of cash value can significantly impact financial planning, offering a flexible tool for managing life's unpredictable expenses.

It's important to note that while accessing cash value can be advantageous, it must be done with a clear understanding of the policy's terms and the potential impact on the death benefit. Professional advice is recommended to navigate these decisions effectively.

Conclusion

In summary, cash value life insurance policies offer a unique combination of death benefit protection and a savings component that accumulates value over time. While these policies can serve as a financial tool for long-term planning, they may not be suitable for everyone. Understanding the intricacies of how cash value accumulates, the types of policies available, and the potential disadvantages is crucial for making an informed decision. If you're considering a cash value life insurance policy, it's important to weigh the benefits against the costs and to consult with a financial advisor to ensure it aligns with your overall financial strategy. For those seeking guidance, our life insurance specialists are available to help you navigate your options and make the choice that best suits your needs.

Frequently Asked Questions

What is cash value in a life insurance policy?

Cash value in a life insurance policy refers to a savings component that is part of permanent life insurance policies. A portion of each premium payment is allocated to this cash value account, where it can earn interest or be invested, growing tax-deferred over time.

How does cash value accumulate in a life insurance policy?

Cash value accumulates in a life insurance policy when a portion of the premium payments is invested by the insurance company into various assets. This can include stocks, bonds, or mutual funds, and the value of these investments grows over time, adding to the policy's cash value.

Can I access the cash value in my life insurance policy?

Yes, policyholders can access the cash value in their life insurance policy through withdrawals, policy loans, or by surrendering the policy. However, accessing the cash value can have tax implications and may reduce the death benefit.

What types of life insurance policies include a cash value feature?

Permanent life insurance policies, such as whole life and universal life insurance, include a cash value feature. This is in contrast to term life insurance, which does not have a cash value component.

Are there any disadvantages to cash value life insurance?

Cash value life insurance policies typically have higher premiums than term life insurance, and accessing the cash value can reduce the death benefit. Additionally, there are fees and potential tax consequences associated with cash value withdrawals or loans.

How do I know if cash value life insurance is right for me?

Determining if cash value life insurance is right for you depends on your financial goals, need for permanent coverage, and desire for a savings component. It's important to consult with a financial advisor to assess your individual situation and consider all potential risks and benefits.

Post a Comment